As I am invited to visit with small and large employers, I am a good listener. What are the ages, wants, budgets and needs of the employees? The employees make the employer successful, so it is ultimate that we consider every aspect of this puzzle. In the end, the numbers will tell the story.

The employer and I begin with some preliminary strategic ideas to contain the skyrocketing costs. When I say that, I mean the premiums and the out-of-pocket expenses. The employees and their families are paying more than ever before as a result of the realities of healthcare in our country.

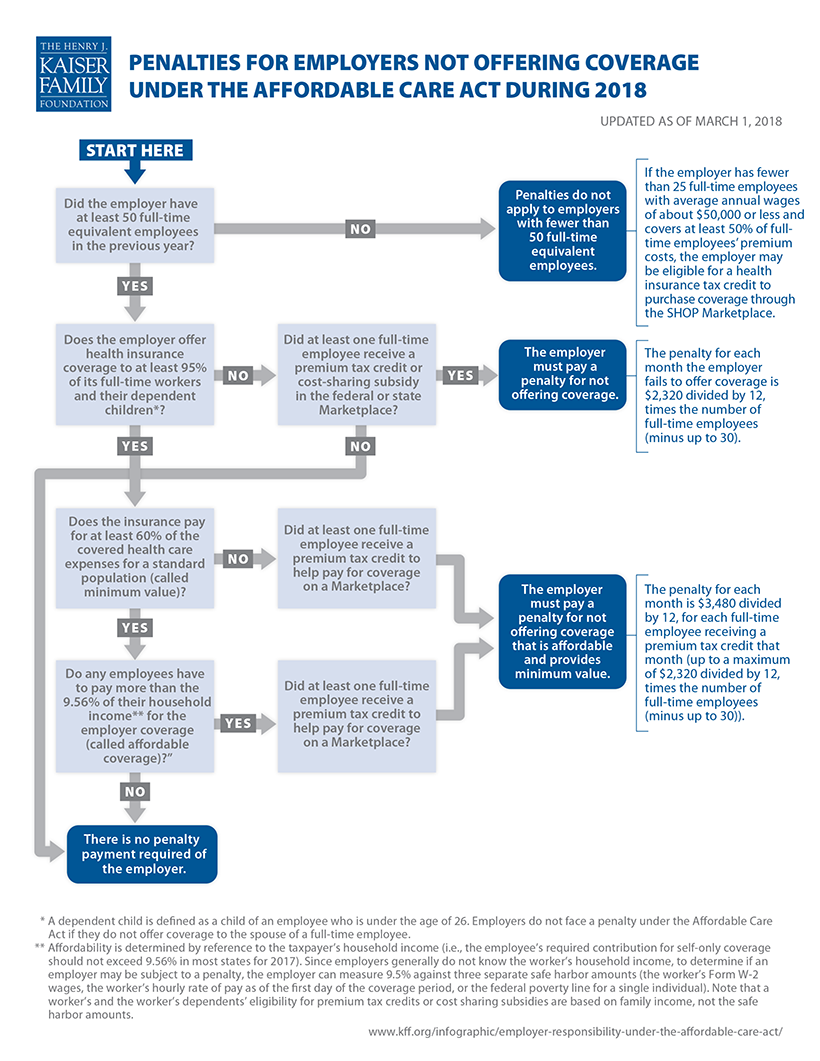

There are three points that I would like to focus on for your consideration:

• The networks of providers that we can access are shrinking along with the formularies on pharmacy items being narrowed. Some plans are leaving families with an excess of 40% of the medical costs. The average outlay is over $11,500, with an approximate $4,500 being out-of-pocket expenses. This illustrates a consistent increase of about $1,000 per year for the last several years. So, you may ask yourself, “How does the rising cost of care and smaller networks affect me?”. Nearly one third of patients are referred to specialists each year. The primary care physician is referring more than ever, in part due to liability. However, 50% of those referrals are out of network. So, the end result is rising premiums, smaller networks and high out-of-pocket costs that are a burden for most employees. I take extra consideration when suggesting network choices based on the known demographics of the group. It is prudent to offer choices, so that there are appropriate network options for all.

• Foregoing care drives even higher costs for the family and the employer-provided medical plan. I encourage high-deductible health plans as a strong option for lower premiums and tax incentives combined with the idea that employees would be better consumers. The risk is that families will forego care, with a noted 55% reduction in office visits. This means that they are skipping both appropriate and inappropriate care. Missing an early diagnosis of a major health issue or failing to maintain an existing condition lands folks in the ER. With a plan like this in place, I take extra steps to provide the tools and education for them to enjoy the benefits of this option. This is a great choice, but some employees would be better off with different choices.

• A large contributing factor of the out-of-pocket expense is the pharmacy utilization. The price increases on prescription drugs is amazingly high and disproportionate. There is an increasing use of specialty drugs which is the fastest-growing component in any medical plan. Most people don’t feel like they have options when it comes to this topic. Removing this benefit from plans to save premium, sometimes proves to be a mistake. I take extra steps to educate your employees to uncover more cost-effective options.

I cannot encourage employers enough to implement health incentives, wellness and fitness programs, tips, blogs, or newsletters. This is important enough that mid-sized to large employer groups are investing in employees dedicated and focused on nothing other than this. What a great way to attract and retain employees. This is a win-win. Investing in family’s health (the bread winner in some cases), the productivity of the employee for the company, and the personal rewards, make a difference.

With the points above being major issues, we offer you 40 years of knowledge and expertise to guide you to wiser decisions. Information is free, but experience is necessary for proper implementation. Please call or email me for an appointment. My consultations are free.

I do not expect an employer or the employees to navigate an industry alone in which they are not trained, experienced or proficient. This industry has also experienced more change, complexities and regulations that ever before.

We are proud to say that our clients have made us successful. One hundred percent of my business is referral. I owe a deep appreciation for the professional confidence that has been placed in me to recommend coverage that is affordable and appropriate for your employees and their family’s needs.

Please visit my Facebook page – Sears Insurance – for weekly blogs and monthly newsletters. If you enjoy what you see, feel free to like us! We are members of the Better Business Bureau and recognized in the industry as Top Producers for decades.

Please visit my site at www.searsinsurance.com to learn more about what we can offer.